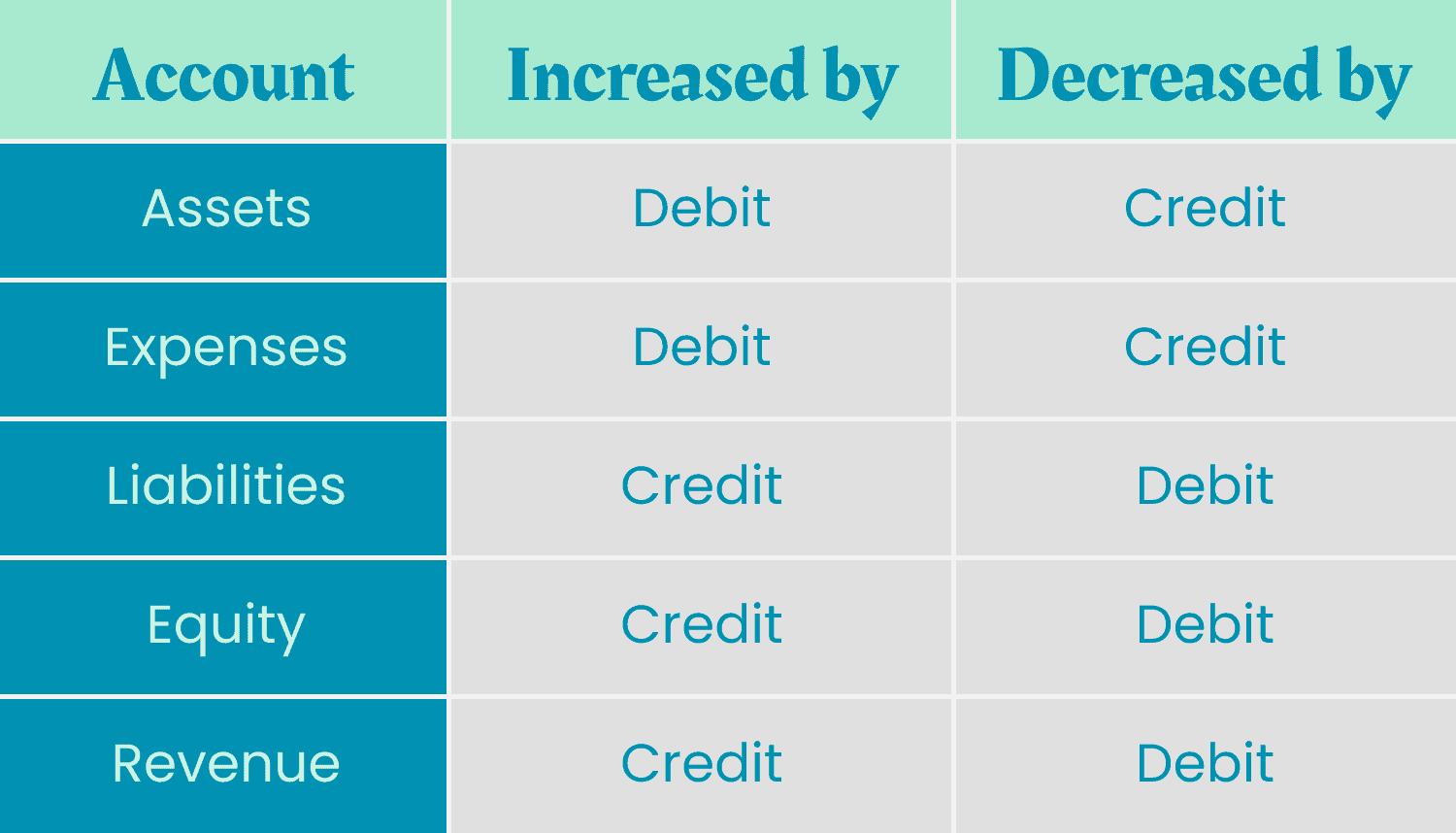

We all already know what debits and credits are. They increase or decrease accounts based on money that you earn and money that you spend. But more specifically, accounts are records that track the financial activities of your small business’ assets, liabilities, equity, revenue, and expenses throughout the business cycle. Simple right?

Not so fast – it’s important to understand the role that account types play throughout the accounting cycle. So before we get going, we’d recommend a quick read on:

- The basics of what an account in accounting is

- Debits and credits in accounting

All set? Good—let’s go!

Arguably, the most important part of bookkeeping is keeping track of your earnings and spending via the two main types of accounts, income and expenses.

Different types of income are taxed differently, and by categorizing your income and expenses, you can optimize the profit margins of your small business.

Related: Manage Expenses: How Truly Small Businesses can Leverage Kashoo, Little Known Tax Breaks for Small Business Owners

There is also a third type of account that we should mention – your liability account. A liability account is used to track things that are basically the opposite of an asset—anything that costs you money to get rid of. The most common liability is credit issued from a vendor or a bank (lines of credit, credit card debt, accounts payable, etc.).

Meet the 5 Account Types

Businesses have many accounts in their books, and nearly every account falls under these five categories:

1. Types of Asset Accounts

Your asset account represents the value of the assets owned by your small business. Only items that have a resale value should be recorded in this account. Every year, those assets will be adjusted to reflect any depreciation or appreciation of their value. Think: furniture, computers, real estate, or inventory!

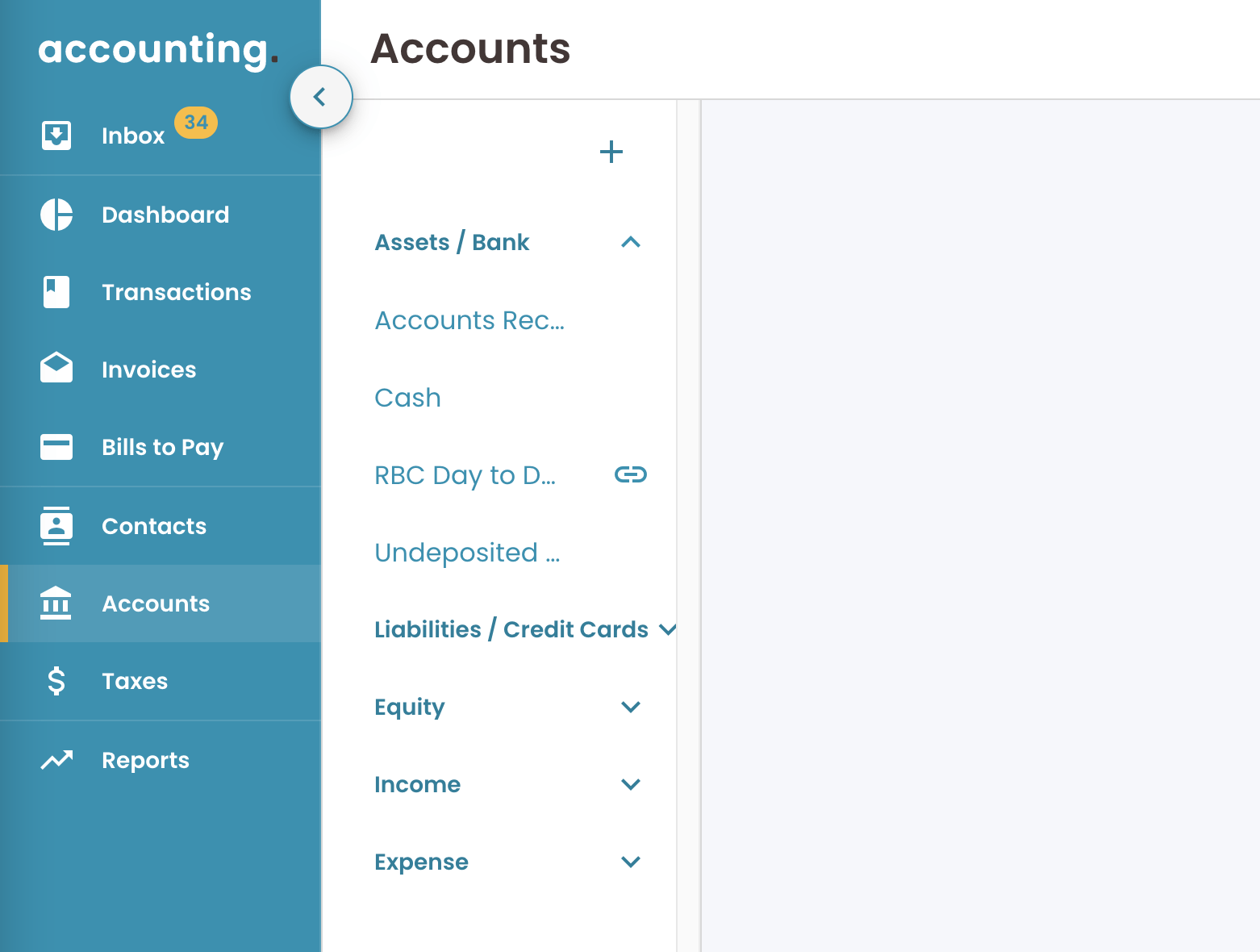

Within TrulySmall Accounting, the first thing you’ll want to do is to set up all of your accounts; so that the moment you purchase or sell any goods or services, you’re able to update your chart of accounts.

Cash Accounts

A cash account is the easiest way to record cash payments, deposits and withdrawals. Cash accounts are handy as they provide a constant picture into your business’ financial health. And cash accounts can come in handy when a small business owner, say, pays for an expense with a personal credit card. In this case, the payment terms will be recorded as cash, since their personal credit card isn’t tracked for business purposes!

In TrulySmall’s Accounting software, we’d reflect this by entering income or expenses received in cash under Terms or Payments Accounts. This will show that you were either paid in cash, or that you paid for something in cash.

Bank Accounts

This account refers to any of the bank accounts that are used for the purpose of running your small business. Think of your checking account that you use for bill payments or incidentals, or your savings account that you contribute money towards in advance of tax season.

(And, if you were wondering – you can find out more about how bank accounts are seamlessly pulled into TrulySmall here.)

Accounts Receivable

Accounts receivable represent the money that is owed to your small business. They generally come in the form of outstanding invoices that are issued by your business, and are payable by anyone you’ve transacted with.

With TrulySmall Accounting, you can create, send, and track invoices, generate detailed reports, and customize your dashboards to more easily navigate the accounting process On the other hand, our invoicing software, TrulySmall Invoices—helps small business owners to seamlessly generate invoices, so that they can stay on top of their accounts receivable.

Undeposited Funds

A common practice is for small business owners is collect cash and checks and deposit them as a lump sum. So, despite the fact that the pool of funds was from multiple sources, the transaction will only be recorded once on your bank statement.

To manage this in TrulySmall Accounting, we’d record the transaction in Undeposited Funds and then transfer the specific amounts of each item from the original deposit into the appropriate account. Eventually, we’ll have to perform a bank reconciliation, and this will allow us to be sure that the transaction date and amounts match corresponding lines on our bank or credit card statements.

2. Types of Liabilities

What are business liabilities? Well, a liability account represents a type of debt or an upcoming cost for the business. And the type of liability determines the duration of the debt.

Accounts Payable

Accounts payable represent money that your small business owes. Accounts payable usually come in the form of bills or invoices from others vendors or service providers.

Credit Cards

A credit card is an indispensable tool for a small business owner. In fact, it is quite normal for a small business owner to have multiple credit cards.

Credit cards are great for keeping tracking of expenses because credit card companies will send you a statement at the end of the month with details of your business expenses. This provides an excellent opportunity for you to check to see if the expenses that you entered into your small business accounting software match up with the entries on your statements.

3. Equity

An equity account represents the net worth and ownership of the business. Examples of these accounts include:

- owner investments (contributed capital)

- retained earnings (owner’s equity in the company)

- common stock (security that represents ownership in a corporation)

4. Income Accounts

Income accounts are used to track sources of income and help small business owners gain insights into where their money is coming from. Generally, the number of income accounts that you’ll have will depend on how many goods or services your business provides. Think of the following:

Habitsoft Inc. began as a custom software development company that also provided consulting services. So, to keep track of their income streams, they set up three different accounts:

- Software Development Income

- Consulting Income

- Interest Income (for interest paid by the bank on any positive balances)

In most cases it’s also a good idea to create an Other Income category for any income that you are having difficulty categorizing. Be sure to consult with your accountant if this is a regular occurence!

Gain or Loss on Foreign Exchange

This account is used to track gains or losses caused by a change in value of foreign currencies, between the time an invoice was issued and the time that it was paid. In TrulySmall Accounting, this account will be displayed in your default chart of accounts. You can opt to use it (or not), depending on whether your business tends to invoice or pay in foreign currency (or not.)

5. Expense Accounts

An expense account represents a category of expenses for the business. Basically, any type of product or service that does not have resale value is an expense. So, if you’re paying for an item that can be resold, be sure to record it as an asset. This is a key aspect in the accounting cycle!

Before setting up your expense accounts it is a good idea to consult your local tax laws as they may have certain categories that you’ll have to adhere to.

When you sign up for TrulySmall’s Accounting software, a list of expense accounts will automatically be included. Be sure to review this list to see if it is aligned with your local tax laws. From there, you can add any expense reporting categories that you feel are necessary.

Cost of Goods Sold

The cost of goods sold are the costs that goes into creating the product that your small business sells. The only costs included here are those that are directly tied to the production of your products.

For example, raw material and labour used to produce a physical product would be included in the cost of goods sold, while the cost of shipping the finished product to the retailer where it was sold, would not.

A Peek Inside TrulySmall Accounting

A default chart of accounts will be provided to you when you begin your small business accounting software process with TrulySmall. This default list represents some of the most common account types used across most businesses. That said, you may want to add or remove particular accounts to suit the needs of your small business’ needs.

Whether you need the ability to accept payments, generate expense receipts, or access to simple invoicing software, trust in TrulySmall’s small business accounting software to help you navigate the accounting cycle with ease.

Conclusion

And there you have it! A high-level overview of the different account types used in an accounting system. As always, if you have any questions about accounting, bookkeeping, or best practices with setting up your chart of accounts—our support team is here to help. Contact us at answers@kashoo.com or on Twitter at@KashooOnline.

*TrulySmall Accounting also offers a 14-day free trial for those of you who want to experience the flexibility and seamlessness of our small business accounting software’s chart of accounts. Try it today to see how easy it is to get set up on the best small business accounting software platform available!

This is the second part in an ongoing series of articles diving into accounts and how they are used in the context of accounting.