Let’s talk about the elephant in the room: Accounting can be hard and at times, quite complex.

But that didn’t stop us at Kashoo to try and build out a software designed to simplify how you run and manage your books. Alongside our goal of trying to make accounting as simple as possible, we have dissected in detail, the anatomy of an income statement.

Let’s Get Started.

What is an Income Statement?

According to the Wiley Dictionary, “An income statement is a financial statement that presents the revenues and expenses and resulting net income or net loss of a company for a specific period of time.”

But what does all this mean exactly?

First, let’s answer two simple questions:

- How much income did your business bring in last year?

- How many expenses did your business incur last year?

If you can answer the above questions, and can calculate your Total Income – Expenses = Profit… guess what? You have just created an income statement!

Essentially, an income statement is where you show how much income and expenses your business has incurred throughout the year. Then, after calculating your Net Income, you can make the decision on whether or not your business was profitable this year.

Understanding an income statement is essential to business owners and investors as it provides an overview of the profitability and future growth of your company. Without knowing whether or not your business is profitable, will most likely prevent you from trying to obtain investors, loans or other complex business arrangements.

Before we dive further into the anatomy of an income statement, here are the alternatives of how an income statement is defined within most financial statements:

- Profit and Loss Report

- The Statement of Income

- The Statement of Earnings

- The Statement of Operations

- The Statement of Operating Results

Each one of the above titles essentially all mean the same thing: The Income Statement.

Basic Income Statement Formula

To simplify your understanding of an income statement even further, here is the basic formula that builds an income statement:

Revenues – Expenses + Other Income/Losses = Net Income

Remember that an income statement records the total activity of the business’ operations throughout a certain period of time. For example, if your business’ fiscal year end is 12/31/15, then your income statement will record its business operations from 01/01/15 to 12/31/15.

Meaning, all sales and expenses that you incurred during 01/01/15 to 12/31/15 will be recorded on your Income Statement for fiscal year-end 2015.

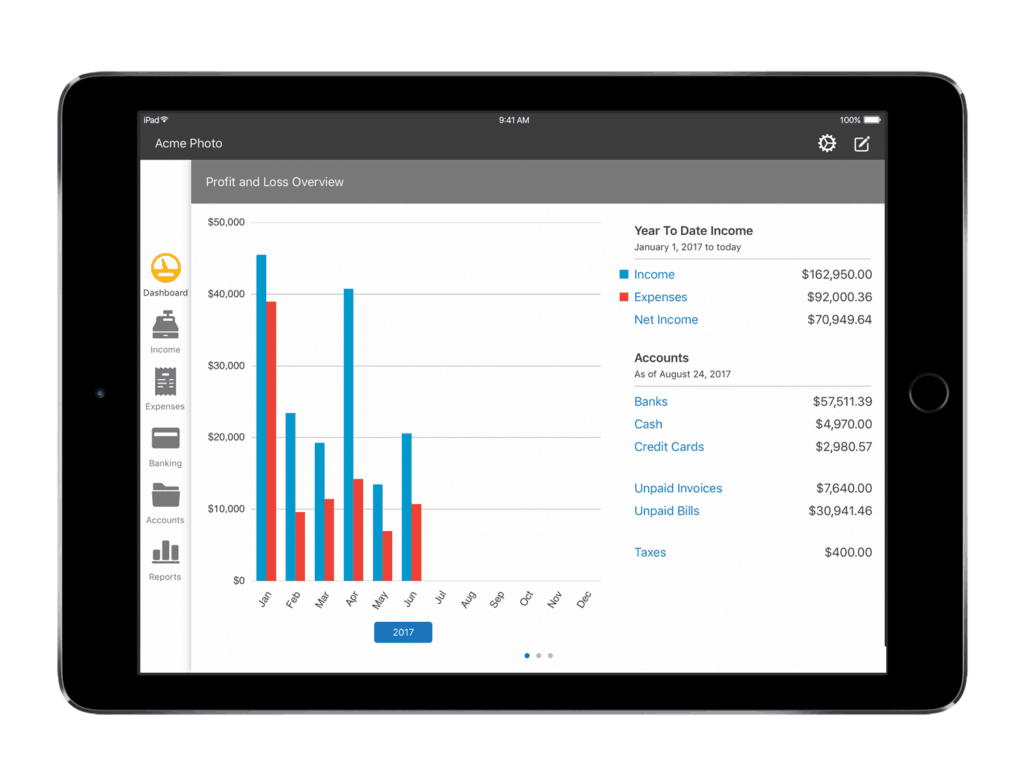

Here is an example income statement from the publicly traded company, Flanigan’s Restaurant extracted from www.sec.gov:

As you can see above, the income statement starts with the total revenue incurred by Flanigan’s, then moves onto the expenses incurred, and finishes off with the other income/expenses incurred throughout the year.

If you are not great at math, no need to worry. Let’s break down this formula into definitions and examples to help give you a better understanding of what you are looking at.

Revenue = Company’s Operating Income

Essentially, revenue is the total sales of goods and/or services you have provided to your customers throughout the year. A great example is if you run a company that distributes bread, your revenue will include the total loaves you sold to your customers throughout the year. Plus, if your business sold different types of bread, you can break out your revenue as follows:

Total Revenue

- Whole Wheat Bread Sales

- Multigrain Bread Sales

- Baguette Sales

Your total revenue, in the bread example, will include the sum of all 3 types of bread sales. Make sense?

Note that the revenue line is at the top of the income statement because it essentially drives the costs and the gain/losses incurred throughout the year.

Here are a few other terms that are used to describe revenue:

- Sales

- Net Sales

- Total Revenue

- Net Product Sales

- Net Service Sales

Expenses = Costs Incurred

Expenses are the total purchases or costs the company has to pay for throughout the year as it relates to the normal course of business.

The income statement can show a breakout of costs per product, or keep it simple by just outlining each cost incurred for the entire business.

Going back to the bread distributor example above, each loaf of bread you sold has a cost attached to it for how much you purchased it for from your manufacturer. Let’s say your manufacturer sold you the bread loaves for $5/loaf. Take $5/loaf and multiply it by the total amount of bread you purchased from the manufacturer, and that is the balance that is included within your Expenses section of the income statement.

Let’s say you are a manufacturing company selling handbags, and it costs you $10 to make 1 bag. Within the manufacturing costs of $10/bag, you have to purchase the materials ($5 in raw materials), pay someone to make the bag ($4 in direct labor), and make the bags within a warehouse ($1 in overhead). All of these costs get summed together and stated on the income statement under Cost of Goods Sold (COGS).

For distributors and wholesalers only (i.e bread company above), the cost of sales (their version of COGS), is essentially the cost it takes to purchase the item from their manufacturers. i.e. A Cake distributor does not have raw materials and direct labor costs, they just have the finished product costs sitting on their income statement.

For service-related businesses, costs of sales represents the total cost of your service (i.e. for most accountants, doctors and lawyers, their billable hour costs).

Here are a few alternatives to the term expenses:

- Cost of Goods Sold

- Cost of Sales

- Total Expenses

- Cost of Products Sold

Revenue – Expenses = Gross Profit

Remember the formula stated above to describe an income statement:

Revenue – Expenses + Other Income/Expenses = Net Income

Well, if you just section off the Revenue – Expenses, the total value equals what we accountants call, the Gross Profit.

A company’s gross profit essentially showcases the difference between the total net sales and the total costs incurred from those sales. Calculating your company’s gross profit helps you to understand how profitable your products actually are, without taking into account items like depreciation, income tax, etc.

Obviously, the greater the gross profit, or gross margin is, the greater the potential is for a positive net income (or bottom line).

Let’s go back to the bread company example. As we previously mentioned, it costs the company $5/loaf of bread, which is included on the expenses section of the income statement. If the company sells the Whole Wheat Bread Loaf for $10, then your gross profit per this one bread loaf equates to:

Whole Wheat Bread Sale ($10) – Cost Of Loaf ($5) = Gross Profit ($5)

Now you know that for every Whole Wheat Bread sales you make, you will record $5 in gross profit that goes straight to your bottom line.

A few terms that are alternatives to Gross Profit includes:

- Gross Income

- Gross Margin (Gross Profit divided by Total Revenue)

- Gross Profit Income

Other Income/Expenses = Operations Outside Normal Course of Business

Other income and expenses are those items that don’t occur during the normal course of business operation.

For example, a Bread Distributor does not normally earn income from rental property or interest from investments, so these income sources are accounted for on a separate section of the income statement. Another great example is the interest expenses incurred from the outstanding debt of the company. As interest expense does not directly relate to the cost incurred when selling a loaf of bread, it is recorded on a separate line item below Revenue & Expenses.

Here are a few items shown on the other income/expenses section of the income statement:

- Interest Expense

- Provision for Income Taxes (may be shown as a separate line item on the income statement)

- Income from Rental Property (outside of the normal course of businesses)

- Foreign Currency Exchange – Loss/Gains

The Bottom Line

Understanding how your business operations flows through the income statement can help give you a better picture of what makes your company profitable and where the losses are coming from.

Remember that income statements vary by company and by industries but they all have a similar formula in how they are displayed:

Revenue – Expenses + Other Income/Expenses = Net Income

Now that you have a better understanding of the anatomy of an income statement, head over to your Kashoo accounting software and start reviewing your own company’s income statement, we call it a Profit & Loss Report! And of course, if you run into any questions, feel free to reach out to answers@kashoo.com. Good luck!

Want to learn more about accounting? Check out the rest of our Kashoo U guides!