Most people are familiar with debit and credit outside the context of accounting. We have debit cards and credit cards that allow us to spend money directly from our checking account (debit cards) or from our line of credit with our bank (credit cards). In this sense, debits are viewed as money drawn from our bank account, and credits are viewed as money available to spend or borrow from the bank. This is how debits and credits are represented on your bank account statement.

However, in the world of double-entry bookkeeping, the definitions and roles of debit and credit are quite different. You will need to understand the difference between the two so that you can use them to keep track of your business transactions across the various types of accounts being used within your business. For an in-depth explanation of the different types of accounts used in accounting, check out “What are the Different Account Types in Accounting?”

Debits and credits in double-entry bookkeeping: the basics

All of your business transactions are tracked as debits and credits (abbreviated as Dr and Cr, respectively) in your account ledger using a T-account, where debits are recorded on the left-hand side of the “T” and credits on the right-hand side. This is actually where double-entry bookkeeping gets its name: each transaction requires both a debit and a credit entry in the account ledger.

The source account, the account where the money for the transaction is coming from, is generally credited on the right-hand side. The destination account, where the money for the transaction is going, is debited on the left-hand side.

In order for a journal entry in the account ledger to be valid, the total debits must be equal to the total credits. In other words, the total entries on the left-hand side of the T-account must equal the total entries on the right. Sometimes, you will need to use multiple debits and credits for a given transaction in order for both sides of the journal entry to be equal.

Let’s take a look at some examples:

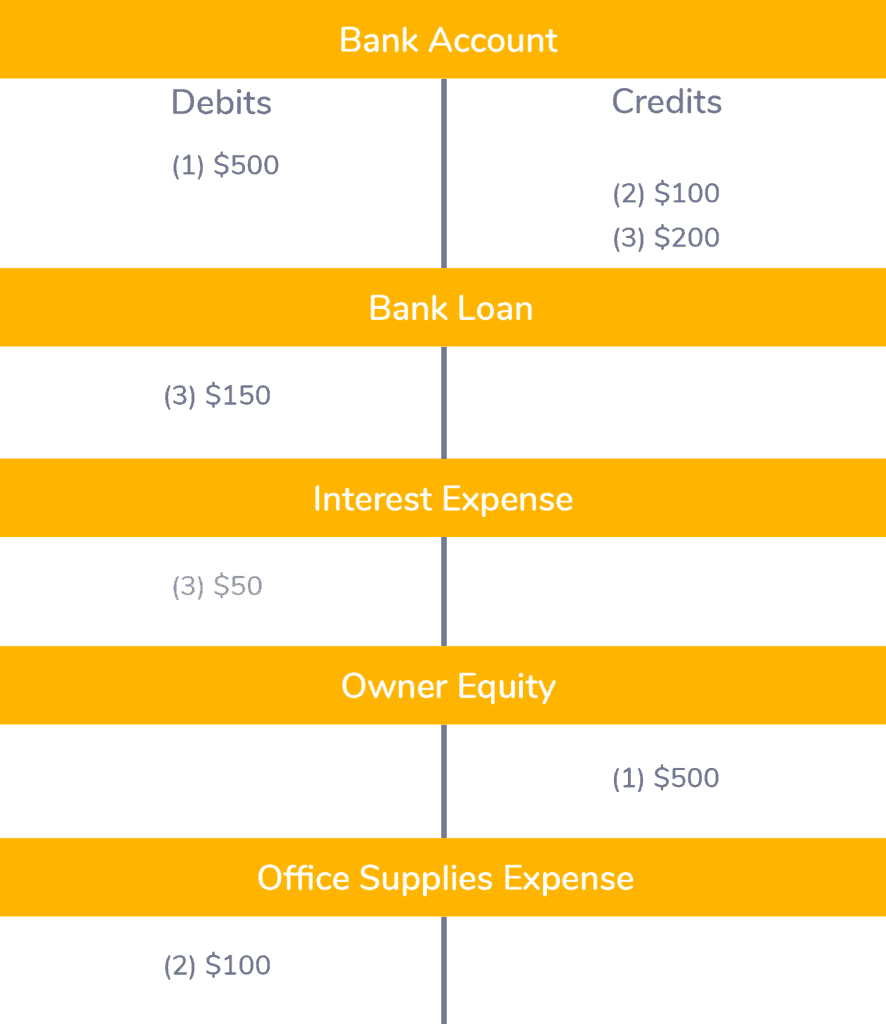

Example 1: As a business owner, you decide to invest $500 into your business. In this case, the source account is the Owner Equity account. Since, as mentioned above, the source account is credited on the right-hand side of the T-account, you will enter the $500 on the right-hand (Credits) side. The destination account in this example is the Bank Account, so you will enter $500 on the left-hand (Debits) side to complete the journal entry.

You can tell that this is a valid journal entry because the total debits ($500 debited from the Bank Account on the left-hand side) are equal to the total credits ($500 credited to the Owner Equity account on the right-hand side).

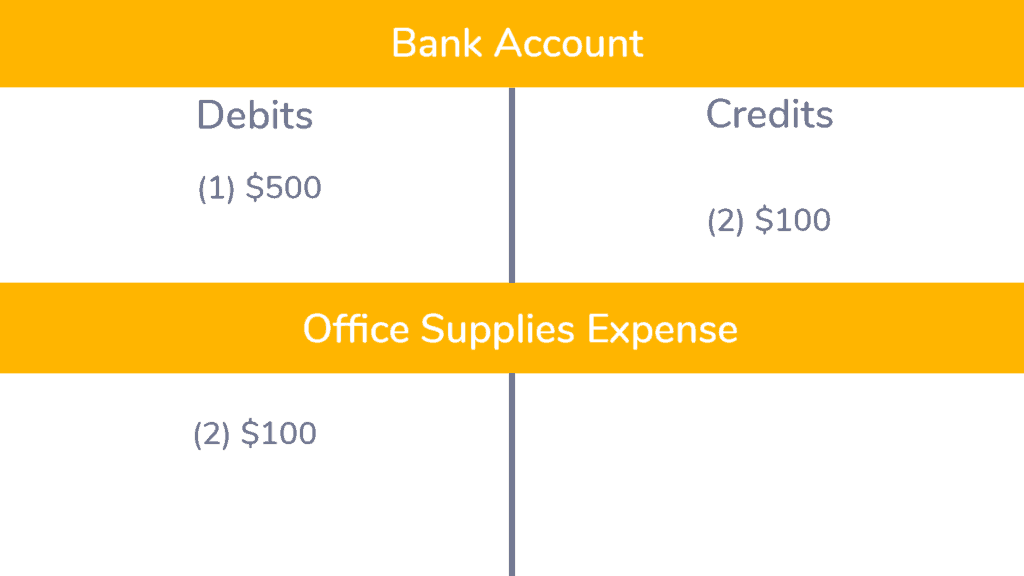

Example 2: Carrying on from Example 1 where you put $500 into your Bank Account, now you have purchased office supplies costing a total of $100 using funds from this account. This means that the Bank Account is the source account, and so $100 will be recorded as a credit on the right-hand side of the T-account. The Office Supplies Expense account is the destination account, which is debited on the right-hand side.

Note: In the T-account above, the transactions making up the first journal entry are labeled “(1)”, and the transactions from the second journal entry are labeled “(2)”.

This second journal entry is valid because the total debits ($100 debited from the Office Supplies Expense account on the left-hand side) are equal to the total credits ($100 credited to the Bank Account on the right-hand side).

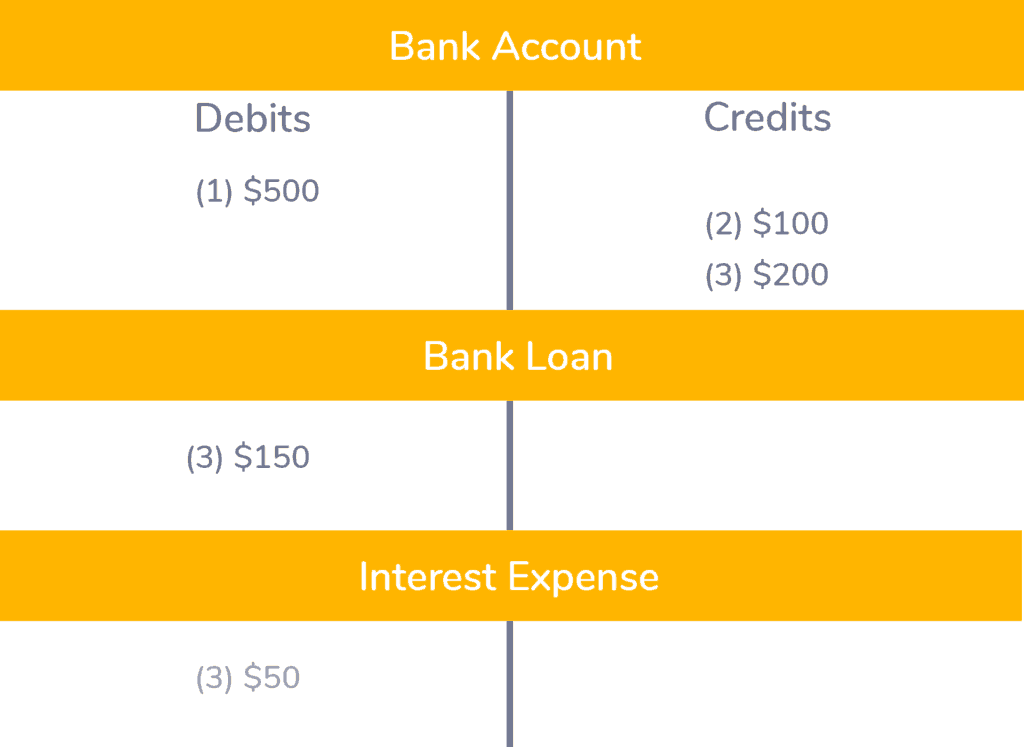

Example 3: Now let’s look at an example where we are required to record multiple debit and credit entries.

You are paying off a loan from the bank using funds from the Bank Account. The payment is comprised of a $150 principal and $50 in interest ($200 total). You will first need to make an entry on the right-hand (Credits) side for $200 for the source account, which in this case is the Bank Account.

The multiple entries come into play because in this case, there are not one but two destination accounts: the Bank Loan account and the Interest Expense account. You will enter a $150 debit under the Bank Loan account, and enter a $50 debit under the Interest Expense account.

The total credits for this journal entry add up to $200, and the total debits add up to $200 ($150 + $50), making this a valid journal entry with multiple debits and credits.

Balances of accounts: What is a debit balance and a credit balance?

An account’s balance is the difference between the total debits and total credits of the account. When total debits are greater than total credits, the account has a debit balance, and when total credits exceed total debits, the account has a credit balance. When the trial balance is drawn up, the total debits must be equal to the total credits across the company as a whole (see below for a sample trial balance). If they are not equal, then you know that an error has occurred.

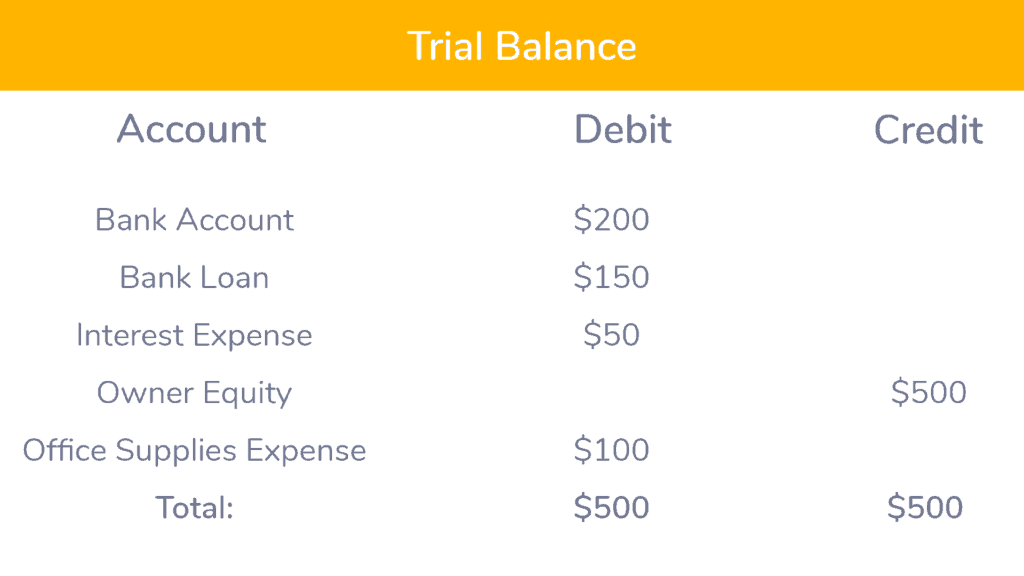

Let’s create a trial balance for the transactions listed in Examples 1-3 above. First, here is a summary of the transactions that will make up the trial balance:

Here is what the trial balance would look like:

The total debits in the trial balance ($500) equal the total credits ($500), as they should. However, you will notice that some of the accounts have a greater number of debits, while others have a greater number of credits. The accounts carrying a debit balance are Bank Account, Bank Loan, Interest Expense, and Office Supplies Expense. The Owner Equity account is the only account carrying a credit balance.

A trial balance is a standard format used by accountants to prepare financial statements (balance sheets and income statements, for example), which allows the company’s financial activities to be shared in an easily understood fashion.

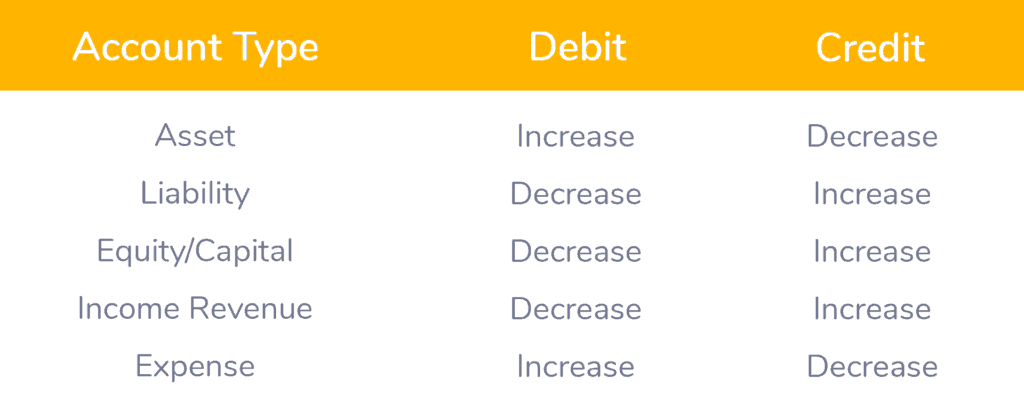

Which types of accounts normally have debit balances, and which have credit balances?

Debit balances generally occur in certain types of accounts, while credit balances generally occur in others. Refer to the chart below for the normal state (“Debit” for accounts normally carrying a debit balance, “Credit” for accounts normally carrying a credit balance) of the five main types of accounts. Again, you can read more about the different types of accounts on our blog here.

Debits and credits in Kashoo

Debits and credits are logged on the Transfers page and Adjustments page (where you can create journal entries) in your Kashoo account. We’ve got articles for both these pages and how to use them in our help database!

A New Way To Track Debit and Credits

We built TrulySmall Accounting to be a simpler way for business owners to track their financial data. Using modern day technology like automation and machine learning, TS Accounting is a fully-automated accounting software that handles all of your debits and credits in the background. Knowing how it works is important, but you shouldn’t have to manage your debits and credits on your own.

To use TS Accounting, all you have to do is connect your bank account and we’ll instantly import and categorize up to a year’s worth of transaction data into your accounting software. The system does everything in the background, so all you’re left to do is make minor edits and check out your financial reports and visual insights dashboard. Your reports and insights will always be up-to-date and you won’t even have to lift a finger.

So those are the basics of accounting credits and debits! Of course, if you have any questions, we’re here to help. Drop us an email at answers@kashoo.com.

Ready to see debits and credits in action in your business? Try TrulySmall Accounting for free for 14 days and see just how much we’ve simplified double-entry bookkeeping for you!

I would like to thank you for the efforts you’ve put in writing this blog.

I’m hoping to iew tthe samne high-grade blog posts from yyou

in the future as well. In truth, your creative writing abilities has

inspirsd mee to get my oown webnsite now 😉

Glad to hear it! Thanks for the support.

None of the images or charts are showing up… so I’m no closer to understanding, but at least I’m not even more confused. That would be impossible.

I’m really enjoying the design and layout of your website.

It’s a very easy on the eyes which makes it much more pleasant for me to come here and

visit more often. Didd you hire out a designer to create your theme?

Fantastic work!

We’re super happy to hear that you’re enjoying our website! Thanks for the support.

Thanks for letting us know! We’ve now fixed all the charts and images so that they should be visible. Sorry for the inconvenience!

Howdy! This is my first visit to your blog! We are a team of volunteers and starting a new project in a community

in the same niche. Your blog provided us valuable information to work on.

You have done a marvellous job!

you’re actually a good webmaster. The web site loading velocity is incredible.

It sort of feels that you’re doing any unique trick.

In addition, The contents are masterpiece. you’ve done a magnificent

process in this topic!

Wonderful blog! I found it while surfing around on Yahoo News.

Do you have any tips on how to get listed in Yahoo News?

I’ve been trying for a while but I never seem

to get there! Appreciate it