As a business owner with a rapidly growing business, you’re never completely clear from lawsuits. Whether it’s infringement or a product issue, unpredictable things happen all the time. In business, this often leads to losses. These potential losses are known as a contingent liability—and if you run a small business or any business for that matter, you’ll need to plan for it and have all the details necessary to report to investors, whether now or in the future.

What Exactly is a Contingent Liability?

Liability is set up as an obligation or a debt. It creates legal responsibility through a lawsuit. Unfortunately, there are many unknowns surrounding liabilities. It’s often difficult to know what the amount of liability will be. Any unknown future potential losses are known as contingent liabilities.

The probability that the contingent liability will become an actual liability

Accuracy of estimating the amount

By definition

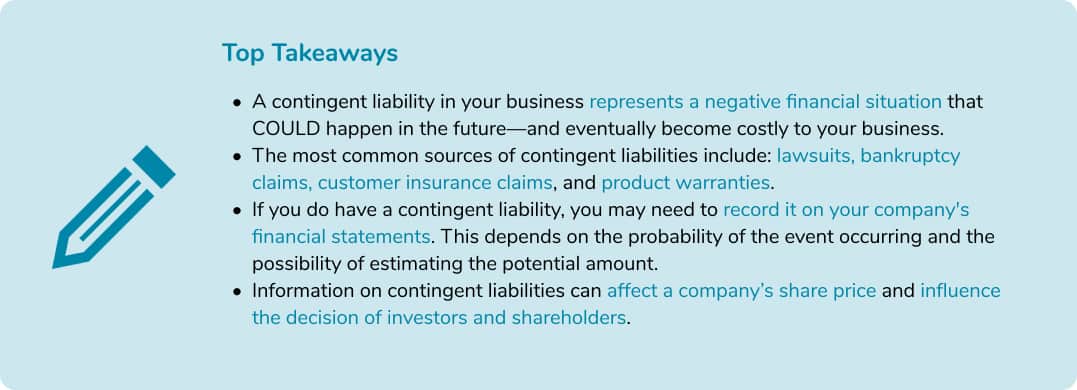

A contingent liability is a liability that may occur depending on the outcome of an uncertain future event. A contingent liability is recorded if the contingency is likely and the amount of the liability can be reasonably estimated. The liability may be disclosed in a footnote on the financial statements unless both conditions are not met.

Contingent Liability Example

Let’s say an employer pays an employee “off the books” in cash and doesn’t report the income or the taxes, or pay the unemployment insurance for this employee. If the employee is laid off and tries to file an unemployment claim, the case may come before a state unemployment board. This creates a contingent liability, because the employer may have to pay an unknown amount for the claim, in addition to fines and interest.

Contingent Liability Types

Contingent liabilities typically fall into these categories:

Product warranties and claims: How many people will have claims? How many will need service or replacement?

Customer insurance claims: How many customers might file claims? What is the claim limit? What if many people file claims?

Employment situations like whistleblower actions or discrimination lawsuits against a company: What might a court decide? How much might the court award the employee?

Claims by creditors in business bankruptcy: How much does the business owe its creditors? How many claims can be settled? What’s the maximum amount?

How Does it Affect Accounting?

Incorporating a contingent liability into your business reporting process is a two-step process:

Recognize the liability. This is where you decide if the contingent liability should be recognized with an accounting transaction created and included in the reports.

Estimate the amount. Next, you then identify the probability of the occurrence and whether the cost of the occurrence can be estimated.

The findings from these two will tell you what’s exactly required when including contingent liability in your financial statements. In some cases, the accounting standards require what’s called a note disclosure (a footnote) in the company’s reports.

Impacts of Contingent Liabilities

As a budding business owner, your mind is busy conjuring up ways to grow fast and enter new markets. One of the tried-and-tested ways to get operations up and running or to expand existing operations is to raise capital through rounds of external funding—also known as Series A, B, and C Funding.

If you intend to seek out these investors, know that potential investors may look at your company’s prospectus as part of the due diligence process, which must include all the information on your financial statements. On your prospectus, investors typically pay particular attention to items that reduce your business’ ability to generate profits, like contingent liabilities.

How to Avoid Contingent Liabilities

Generally, contingent liabilities can’t be avoided. As an operating business, you’re always at risk for unpredictable occurrences. Something as simple as a slight shift in usual weather patterns could create unforeseen losses for your retail business, say if your shipment’s delivery depends on good weather.

Though you can’t avoid them completely, there are ways to deal with them proactively. You can:

Avoid taking payment for goods or services on credit or a client’s word. Instead, ask for payment upfront as much as possible during invoicing. This is especially the case if you have performed your part of the scope, as agreed upon beforehand.

Always record contingent liabilities in your books. Record keeping is a must for small business owners, and recording contingent liabilities in your business’ accounting books is one of them! While the amount might not be completely determined, you can still avoid errors by at least making note that the company might have a pending debt.

Make payments in full. If you can afford it, try to make payments in full rather than installments. While this is not always feasible in all cases, avoiding future installment payments can eliminate more issues associated with the payments.

Free Kashoo Insights + Newsletter

Previous PostCapital Receipts vs. Revenue Receipts: What's the Difference?

Next PostStarting and Growing a Profitable Freelance Writing Business