As a small business owner, you and your business’s accounts receivable should be best friends. You should know how your accounts receivable is doing, just like how you would keep tabs on the state of someone close to you! This is important because it determines whether you have enough cash on hand to pay the bills, source more products or invest in areas of your business to grow. After all, the money you earn can’t truly be counted as revenue until you’ve actually collected it from your clients.

What is the Accounts Receivable Turnover Ratio (ARTR)?

The ARTR measures how effective your business is at converting its accounts receivable into money in the bank. The higher your ARTR, the more cash your business has available to pay for expenses and debts. If it’s low, it’s a warning that you need to improve your collection processes or maybe that you need to find more dependable clients.

Here’s how to do it:

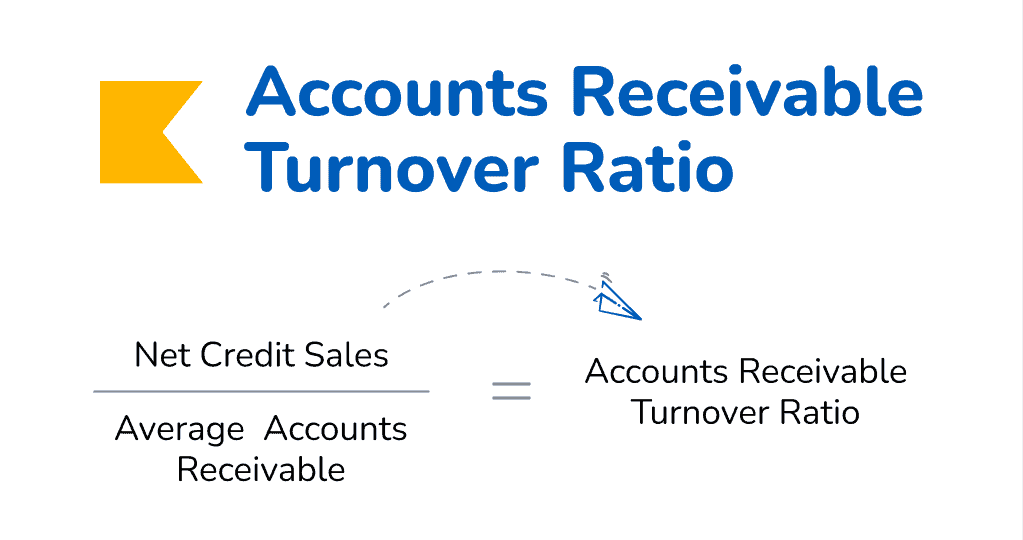

Calculating Accounts Receivable Turnover Ratio (ARTR)

The mighty formula for calculating the accounts receivable turnover ratio is dividing your net credit sales by your average accounts receivable.

Let’s start with net credit sales

Your total credit sales for the accounting period being measured (monthly, quarterly, and annually), less any customer returns and refunds, is what makes up your Net Credit Sales amount.

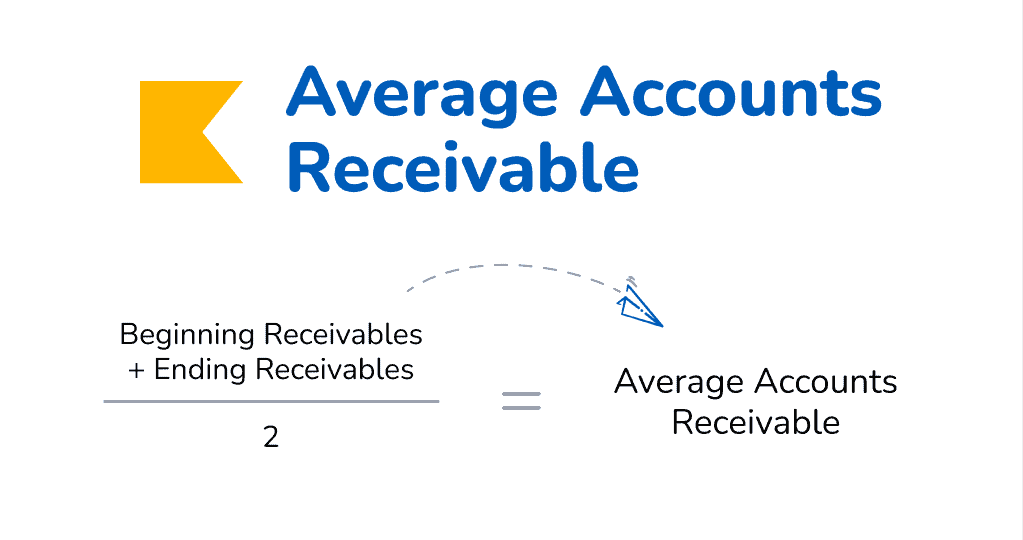

Then calculate your average accounts receivable

You can calculate your Average Accounts Receivable by adding your accounts receivable amount from the beginning of the period to your accounts receivable amount at the end of the period and dividing the result by two.

It’s important to keep both measurement periods the same.

How To Improve Your Accounts Receivable Turnover?

Now that the technical stuff is out of the way, let’s get into the important bits. If your small business is currently struggling with acquiring dependable clients or ineffective collection processes, just know that there are ways to get past this hump. From strengthening strong client relationships to refining your invoicing process, like payment terms, you can absolutely improve your ARTR!

Discover the 8 tips to improve your accounts receivable turnover.

Strengthen client relationships

You can’t avoid relationship building when it comes to accounts receivable. After all, happy customers translate to happy paying customers. Whether you’re a freelancer or a growing company with multiple team members, gestures like email check-ins, friendly phone calls, and even client meals every so often that involves personal chats in addition to business make a huge difference in strong client relationships. For example, remembering a small detail, like a client’s son’s graduation and checking in on that, could help strengthen your relationship with the client. Of course, it’s not only about remembering the small details — it’s really about being a kind and thoughtful human because you want to. From there, the relationships will build themselves. It may not seem like it from the onset, but it could make a big impact for collecting payments.

Invoice accurately and on time

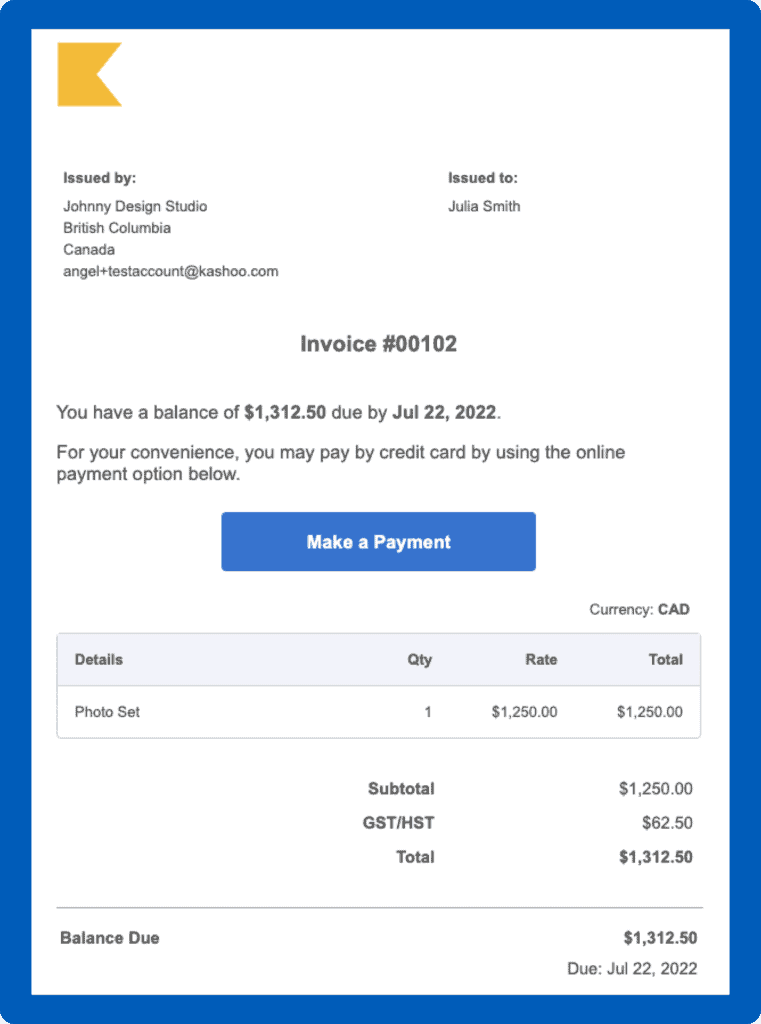

Once relationships are strong and sustained, it’s time to switch focus to invoicing. A detailed and accurate invoice is the easiest invoice for clients to pay. Consistency can a long way here. Make each invoice as detailed and thorough as it needs to be — poorly written invoices can be a breeding ground for miscommunication and confusion, causing clients to slow payment or not pay at all.

Each invoice should generally look the same and include elements such as the date, invoice # (for internal tracking), description of services, and more.

Include payment terms, keep them short, and be strict

The backbone to getting payment on time, every time is through clear payment terms. If you send your first invoice to a new client and request payment each month within Net 30 days, then keep it consistent each month. The terms should also be clearly stated on your invoice.

If cash flow is an issue, you could also consider shortening payment terms — say within Net 15 days. This, of course, would have to be confirmed ahead of time with your client.

And don’t be afraid to include late payment charges. Late payment fees are usually charged as a percentage of your original invoice amount. Alternatively, a flat fee could work too (say, $15 fee for an unpaid invoice under $200). A general late fee for invoices among freelances charges roughly 1.5% monthly interest fees for late invoices, according to Keeper Tax.

Provide discounts for early payment

Another way to fast-track payments — or at the very least, keep them on time each month — is to offer discounts to incentivize payments. For example, you could set your payment terms to be 1% 10 Net 30, which entitles your client to a 1% discount on the invoice if payment is made by day 10 of invoice date. Clients who happen to be looking to reduce costs might be more inclined to maximize this discount and boost your cash inflow in a short time span. However, keep in mind incentivizing early payment might come at a cost but the cash inflow and time saved on collections could outweigh the cost of the discount.

Use cloud-based accounting software to keep track (like Kashoo)

Cloud-based accounting software gives small business owners all the tools they need to make double-entry accounting streamlined, intuitive and most importantly, fun (well, more like actually enjoyable). From detailed reporting and customization to managing your bookkeeping through a simple, highly intuitive user interface, accounting software offers all the functionality that can help you keep your accounts receivable turnover ratio as high as possible — aka, more money in the bank.

That’s because not only does it help you keep track of all income and expenses according to CRA/IRS standards, but its extensive reporting helps pinpoint important numbers that you would need to calculate ARTR. Apart from the balance sheet, accounting software like Kashoo allows you to pull your Profit & Loss statement (P&L) quickly to identify the net credit sales number needed for the formula.

Make paying invoices easy with digital payments

Gone are the days when the only way to send and accept payments are through cheques or wire transfers. Today, most businesses, small or large, accept many forms of digital payments like electronic fund transfers (ETFs) and credit card payments.

Depending on the size of your business, you have multiple payment tools at your disposal:

TrulySmall Invoices: for the really small businesses who need to send a couple of invoices each month, Truly Small Invoices is a quick and easy way to send invoices and receive payments. Get paid faster with no fees by leveraging TrulySmall’s Pay Now button on your invoice.

TrulySmall Accounting: for a smaller business who only needs to track invoices and expenses, TrulySmall Accounting allows you to accept digital payments. Enable payments by connecting your stripe account, and offer a variety of different digital payment options right on your invoice! It also comes full circle: once the transaction is cleared, each payment is automatically logged in TrulySmall Accounting, making bookkeeping that much easier through automation.

Kashoo Accounting: for a meatier, double-entry accounting software option, Kashoo’s accounting software offers Kashoo Pay: a payment feature that offers seamless click-to-pay invoices to help you get paid faster and with more security.

By offering flexible payment options, you make it easy for clients to pay you, which in turn, increases your accounts receivable.

Follow up regularly

Managing the collection process is never easy or fun. The first part of success is sending detailed, accurate invoices with clear payment terms. The latter part is to provide a friendly nudge, where possible. You can send a friendly follow-up by email or phone:

Hi [name],

Hope your day is going well. Just sending along a friendly reminder of payment for [invoice #] sent on [date]. The invoice is due in one week’s time.

Thanks, and have a great day!

By following up regularly, you’re more likely to increase on-time payments. And, who knows: your client might appreciate it too.

Reconcile your books frequently for up-to-date info

Frequent bank reconciliations are a win-win outcome for any small business. After all, it’s twofold:

- The sooner you reconcile and categorize your business expenses, the more accurate your financial numbers are — giving you a clearer picture of where your business currently stands

- The sooner you reconcile outstanding invoices as you receive payment, the more accurate your accounts receivable balance is — making it easier to track ARTR.

If the idea of bank reconciliations has never been appealing to you, then consider accounting software that automates the reconciliation process. TrulySmall Accounting offers a smart inbox with a new Auto Posting feature. When enabled through settings, you can sit back, relax and let the smart accounting software categorize and post your transactions for you.

The caveat? Make sure to still do a weekly review of all posted transactions to ensure all transactions are categorized and detailed correctly. Over time as you fix and apply transaction rules, the Smart Inbox learns over time and helps make each weekly review that much shorter. It’s a win-win!

A healthier accounts receivable turnover ratio = a healthier business

The bottom line is simple. Making the effort as a business owner to manage, track and optimize accounts receivable turnover is crucial for an overall healthier business cash flow. From spotting trends in your accounts receivable practices to understanding the impact of invoicing well, your business’s profitability and long-term revenue growth hinge on these day-to-day habits.

Invest in smart accounting software today to streamline this process!